The SECURE Act’s “10-year rule” is widely understood to mean that non-spouse beneficiaries have a decade to empty an inherited IRA. What is far less understood — and far more consequential — is that for many beneficiaries, waiting until year 10 is not an option. Annual distributions may be required along the way. Missing them triggers penalties. And most families have no idea.

“I inherited an IRA, so I can just leave it alone for 10 years and withdraw it at the end.”

This assumption is correct for some beneficiaries in some circumstances. It is dangerously wrong for many others — and it is precisely the kind of oversimplification that produces avoidable IRS penalties and unnecessary income tax acceleration.

‘Whether a beneficiary can defer all distributions until year 10 — or must take annual required minimum distributions (RMDs) in years 1 through 9 and then fully empty the account by the end of year 10 — depends on two questions that most beneficiaries never think to ask.

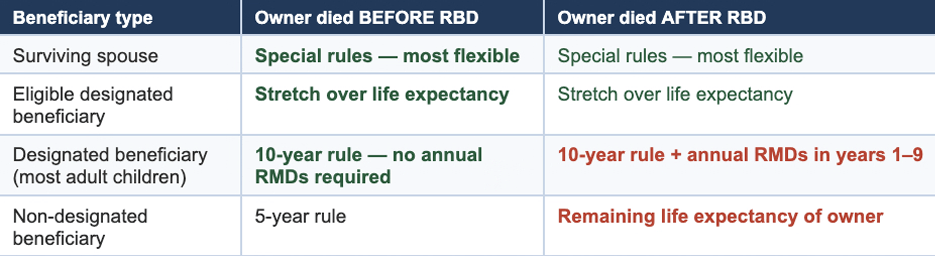

The SECURE Act created distinct categories of beneficiaries, and the payout rules are different for each:

Has unique flexibility, including the ability to roll the inherited IRA into their own IRA and defer distributions based on their own age.

Includes minor children of the original owner, disabled or chronically ill individuals, and beneficiaries not more than 10 years younger than the original owner. EDBs may stretch distributions over their own life expectancy.

Most adult children and other named beneficiaries fall here. Subject to the 10-year rule — but whether annual RMDs apply depends on when the original owner died relative to their Required Beginning Date.

Estates, certain trusts, and charities. Subject to a 5-year rule if the owner died before the Required Beginning Date, or the remaining life expectancy rule if after.

The Required Beginning Date (RBD) is generally April 1st of the year following the year the original owner turned 73. This date determines whether a designated beneficiary must take annual RMDs during the 10-year period or can wait until year 10.

The highlighted cells in red are where compliance failures happen. A designated beneficiary who inherits from an owner who died after the RBD and simply waits until year 10 to withdraw everything has been missing annual RMDs for nine years — each one a separate IRS penalty event.

The question is never simply “do I have 10 years?” The real question is whether annual distributions are required during those 10 years — and the answer depends on who you are as a beneficiary and when the original owner died relative to their Required Beginning Date.

An IRA Inheritance Trust — sometimes called a retirement trust — is a specialized trust designed to receive inherited IRA assets. When properly drafted, it can serve as the designated beneficiary of an IRA, with a trustee administering the account under the trust terms rather than leaving distribution decisions to an individual beneficiary.

The trust’s most practical benefit is administrative: it places a trustee — not an inattentive or inexperienced beneficiary — in charge of ensuring the account is managed correctly. Annual RMDs are taken when required. Distributions are made according to the trust terms. Compliance failures are far less likely.

But the trust is most valuable when the risk isn’t the tax rule itself — it’s the beneficiary’s ability or willingness to follow it. A retirement trust is worth serious consideration when the intended beneficiary is:

The trust is most often considered when retirement assets are substantial and one or more of these factors applies to the intended beneficiaries. For straightforward situations with financially responsible adult beneficiaries, a direct beneficiary designation is often simpler and equally effective.

Founder, The Estate Planning & Elder Law Firm

The SECURE Act, enacted in 2019, eliminated the “stretch IRA” for most non-spouse beneficiaries. Under the 10-year rule, most designated beneficiaries must fully distribute the inherited IRA by the end of the 10th year following the year of the original owner’s death. Whether annual RMDs are required during that period depends on whether the original owner died before or after their Required Beginning Date.

The Required Beginning Date is generally April 1st of the year following the year the IRA owner turned 73 under current law. It is the date by which the original owner was required to begin taking their own RMDs. Whether the owner died before or after this date significantly affects the distribution obligations of most non-spouse beneficiaries.

It depends. If you are a designated beneficiary and the original owner died before their Required Beginning Date, you generally can wait until year 10 without taking annual distributions. If the original owner died on or after their RBD, annual RMDs are typically required in years 1 through 9, with full distribution by the end of year 10. Getting this wrong triggers IRS penalties.

Missing a required minimum distribution from an inherited IRA triggers an excise tax — currently 25% of the amount that should have been distributed, reduced to 10% if corrected in a timely fashion. Each missed RMD is a separate penalty event. For beneficiaries who mistakenly believe they have a full 10 years with no annual obligation, the cumulative penalties can be significant.

It can, if the trust isn’t drafted correctly. For a trust to qualify as a designated beneficiary — and thereby preserve access to the 10-year rule rather than triggering the less favorable 5-year rule — it must meet specific IRS requirements. A retirement trust must be carefully drafted with these rules in mind. An improperly drafted trust can produce worse outcomes than a direct beneficiary designation.

Not always — and the answer depends heavily on who your beneficiaries are and what risks you are trying to address. For financially responsible adult beneficiaries with no creditor concerns, a direct designation is often simpler and equally effective. A retirement trust adds the most value when beneficiaries are young, financially inexperienced, exposed to creditor or divorce risk, or receiving government benefits. We review each client’s specific situation before making a recommendation.

Whether you’ve recently inherited an IRA and need to understand your distribution obligations, or you’re planning your own estate and want to make sure your retirement assets are handled correctly, a first conversation is straightforward. No obligation — just clarity.